GLP J-REIT Characteristics

Utilization of Strong Banking Relationships of GLP Group

We plan to form strong banking relationships by leveraging the existing relationships of GLP Group and to diversify our funding sources by considering multiple financing options, a mix of fixed-rate and variable-rate borrowings, the diversification of maturities and other conditions.

Financing and Cash Management

We intend to form diversified and balanced banking relationships and to diversify maturities for our borrowings in order to establish a stable financial condition in the medium to long term. We plan to diversify our funding sources for the stabilization of loan-to-value ratio, or LTV, and our financial costs.

- LTV Benchmark

- We intend to maintain a target LTV of 45% to 55% in order to operate with a stable financial condition, with a maximum non-binding LTV benchmark of 60%

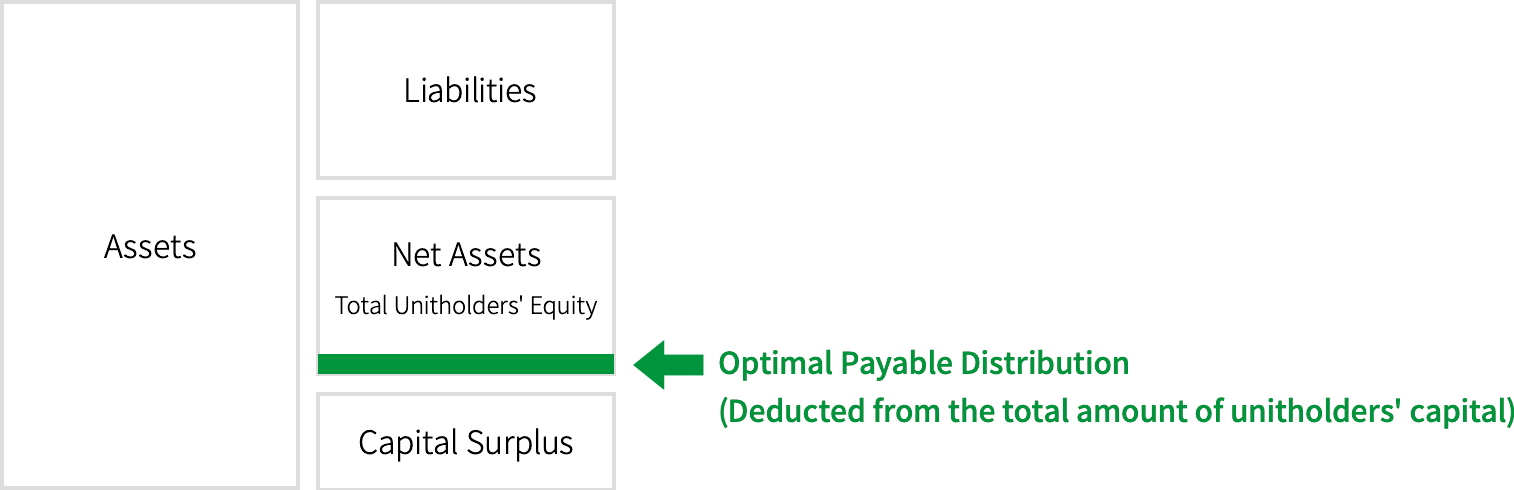

Optimal Payable Distribution

(1) Optimal Payable Distribution

We plan to implement a cash management policy that leverages the characteristics of our logistics properties,(Note 1)and we have a policy to make distributions in excess of our retained earnings (return of capital for Japanese tax law purposes) at the end of each fiscal period on a continuous basis. We refer to the portion of distributions that exceeds our retained earnings as the "optimal payable distribution" portion. We will make such distributions in accordance with the following policy for the purpose of implementing the optimal payable distribution policy centering on efficient capital allocation, in addition to the cash distributions from retained earnings.

(2) Temporary Distribution in Excess of Retained Earnings

We may make distributions in excess of retained earnings (return of capital for Japanese tax law purposes) for the purpose of stabilizing the level of distribution per unit in cases where the amount of distribution per unit is expected to decrease temporarily to a certain degree due to financing such as issuance of new investment units, incurrence of loss on retirement of buildings or equipment, incurrence of significant repair costs or others reasons, in addition to the optimal payable distribution as described in (1) above. Provided, however, that such distributions in excess of retained earnings shall not exceed the amount prescribed under the rules of The Investment Trusts Association, Japan, together with the amount of the optimal payable distribution portion as described in (1) above.

- The amount of the distribution in excess of retained earnings (return of capital for Japanese tax law purposes, i.e., distributions from capital other than the allowance for temporary difference adjustments. The same applies below.) made to our unitholders during any given fiscal period shall be such an amount as is determined by us, which will not exceed the amount of depreciation expense posted for the immediately prior fiscal period, less than the amount of capital expenditures for the same fiscal period. (Note 2)

- The distribution and the amount of the above-mentioned optimal payable distribution portion and temporary distribution in excess of retained earnings shall be determined with sufficient attention given to the amount of capital expenditure, our financial conditions (especially to LTV benchmark)(Note 3) and other relevant factors. If we deem it inappropriate to make such distribution taking into account a range of factors, including the macroeconomic environment and real estate market conditions as well as our portfolio and financial conditions, we will not make such distribution.

- Logistics facilities have the characteristic that the amount of the actually required capital expenditure is less than the recorded amount of depreciation expense and the estimated amount of capital expenditure may be relatively accurate.

- For the time being, we intend to make distributions of the optimal payable distribution portion as described in (1) above in an amount equal to approximately 30% of our depreciation expense unless we determine that payment of such portion would have a negative impact on our long-term repair plan or our financial conditions in light of the estimated amount of capital expenditure for each fiscal term based on our long-term repair plan.

- This means the ratio of interest-bearing debt to our total assets. We will not make any optimal payable distribution if the appraised value of LTV generated by the following formula exceeds 60%:

Appraised value of LTV (%) = A / B x 100 (%)

A = Sum of (i) outstanding interest-bearing debt (including long-term and short-term bonds) at the end of the fiscal period and (ii) released security deposits at the end of the fiscal period

B = (i) total appraisal value or surveyed price of our properties at the end of the fiscal period, plus (ii) outstanding cash and deposits at the end of the fiscal period, less (iii) expected distributions out of retained earnings, less (iv) expected total amount of the optimal payable distribution portion

Please note that the expected distributions out of retained earnings and the expected total amount of the optimal payable distribution portion shall be based on the figures recorded for the most recent fiscal period.

The following chart illustrates the impact of the distribution in excess of retained earnings:

The foregoing is merely an image and does not show the percentage, etc. of the distribution in excess of retained earnings to the net assets in the balance sheet. In fact, the amount of distribution in excess of retained earnings would change or may not be made, depending on a range of factors, including the macroeconomic environment and real estate market conditions as well as our portfolio and financial conditions.

(3) Distribution in Excess of Retained Earnings Corresponding to Allowance for Temporary Difference Adjustment

We may make distributions in excess of retained earnings in cases where the amount of the allowance for temporary difference adjustments increases, in addition to the distributions in excess of retained earnings as mentioned in (1) and (2) above.